🔄

What online doctor consultation actually means in India today

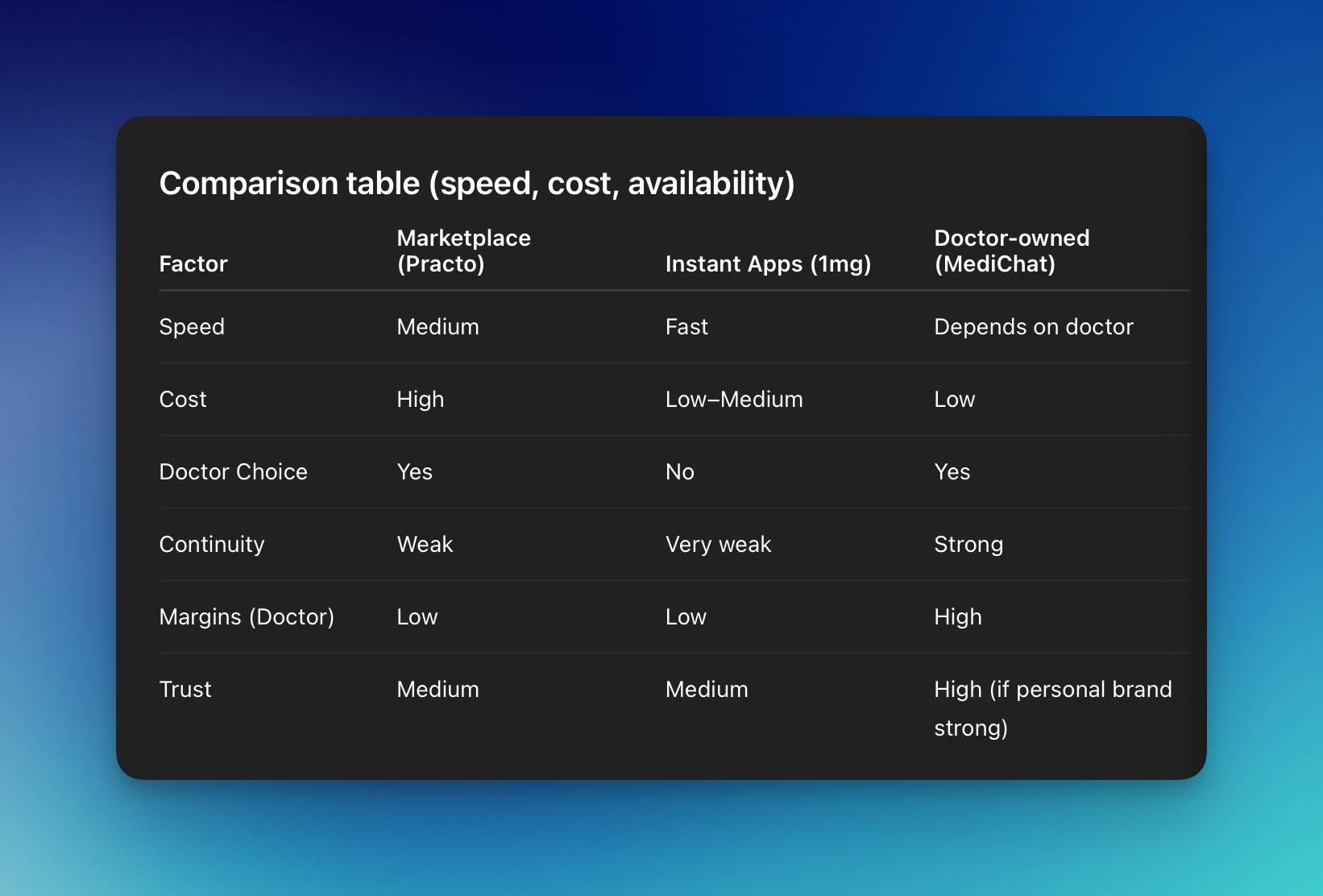

Most people assume that a telemedicine consultation application is basically about talking to a doctor over a video chat, which is outdated in 2026. In India today, online consultations typically fall into three buckets. Usually, they come across the following three buckets, which are marketplace driven consultation platforms such as Practo and Apollo 247. In these platforms, patients usually browse a list of all the available doctors in their area. They pick one of the doctors depending on the reviews, ratings, and the cost of the consultation. They pay the doctor, and the consultation happens.

Secondly, we have instant general practitioners or the pooled doctor model. Platforms such as Tata 1MG, where you do not choose the doctor, automatically assign a doctor to the patient as soon as they hit the consult now button. Here, the system is in the front seat, assigning a doctor for the patient. It is optimized for speed, but not continuity. The problem is that the patient always gets a new doctor every time they have an issue.

Thirdly, there are doctor owned telemedicine setups. These setups are usually configured using a basic EMR style dashboard, a basic payment system, and a communication channel, mostly WhatsApp, because in India, 95 percent of people use WhatsApp as their daily mode of communication. Tools such as Medichat basically cater to this bucket of doctors and patients, where doctors have high control and the lowest platform dependency.

One thing that is clear, and comes as a reality check, is that 70 percent or more of consultations are chat first, not video. Usually, doctors do not like to have video consultations with patients because they feel it does not justify their time, and video quality, depending on internet speed, may hinder the quality of diagnostics, which can lead to false positive information at the time of writing a prescription.

Secondly, follow ups happen outside the platform. Usually, WhatsApp is used as the communication channel, which is where the leakage happens. Finally, platforms are acquisition engines, they are not care ecosystems. What this means is that the cost of acquiring a customer is too high, because they spend a lot of money on Google Ads to acquire users. When customers are onboarded onto the platform, they have to take a cut from the patient, which is on top of the consultation fee. This markup costs a lot for both doctors and the platform.

That is the reason why, whenever a new patient comes to the platform, depending on whether it is a tier two or tier three city, they feel that the cost is too high for the quality of consultation given by the doctor. As a result, it does not become a care ecosystem. Patients do not want to come back the next time. They usually prefer to go to the nearest clinic to get a good consultation at a much lower cost.

How it works step by step (real flow, not theory)

Let's break down the patient journey in reality

-

Intent trigger

Depending on the type of patient, they might have a different intention to use the online consultation platform. They may prioritize this setup if they have mild symptoms, are looking for convenience, or want to avoid clinic wait times. They basically do not want to sit in a waiting room for a long time. On the other hand, late night usage is huge. This is where online consultation applications excel. It is usually during the time between 10 pm to 2 am. It is seen that there are large spikes in the number of consultations recorded in the system.

-

Platform entry

Patients usually search for the platform on the App Store, install the application, and then search for the symptom category. It is seen that most drop offs happen during this stage due to high friction. They not only search for the application on the Play Store or App Store, but also check the reviews and ratings from previous patients who have used the application. If the reviews and ratings are good, they move forward. If not, it creates cognitive overload before they decide whether to install the application.

Next, between installation and finding the right symptom, they have to install the app, sign in, provide details during onboarding, and grant permissions such as location access. Only then can they move to the symptom category phase. That is why we see a lot of friction here.

-

Doctor selection

Now comes the most important phase, which is filtering the type of doctor based on a couple of criteria, such as consultation fees, ratings and reviews, and the experience of the doctor. This usually happens in marketplace type platforms like Practo.

In contrast, instant consultation platforms like Tata 1MG skip this entirely, so the patient does not have a choice. This is where a major trade off happens. More choice increases trust, but reduces conversion speed.

-

Payment first, always

Usually, the payment ranges between ₹200 rupees to ₹800 rupees, which is the typical consultation fee range. Most apps in the marketplace ask for payment first, and only then does the consultation happen.

-

Consultation layer

Although many applications offer both video and chat features, doctors usually prefer chat, and sometimes a call. Video is rarely preferred because the quality of diagnosis depends heavily on internet speed, infrastructure, and clarity of information.

For example, if a patient comes in with a dermatology issue, it is very hard for a dermatologist to determine the actual problem unless a clear image is provided. Over video, this becomes difficult. This is something most doctors agree on. Doctors also tend to multitask across patients, which leads to loss of context between consultations.

-

Prescription plus upsell

Prescriptions are usually sent via email or as a PDF on WhatsApp. On top of this, platforms promote add ons such as lab tests and medicines. This is where platforms make most of their revenue.

-

Follow up leakage

This is where a lot of drop off happens. Patients move to WhatsApp for follow ups. The platform loses long term retention and also loses patient context over time.

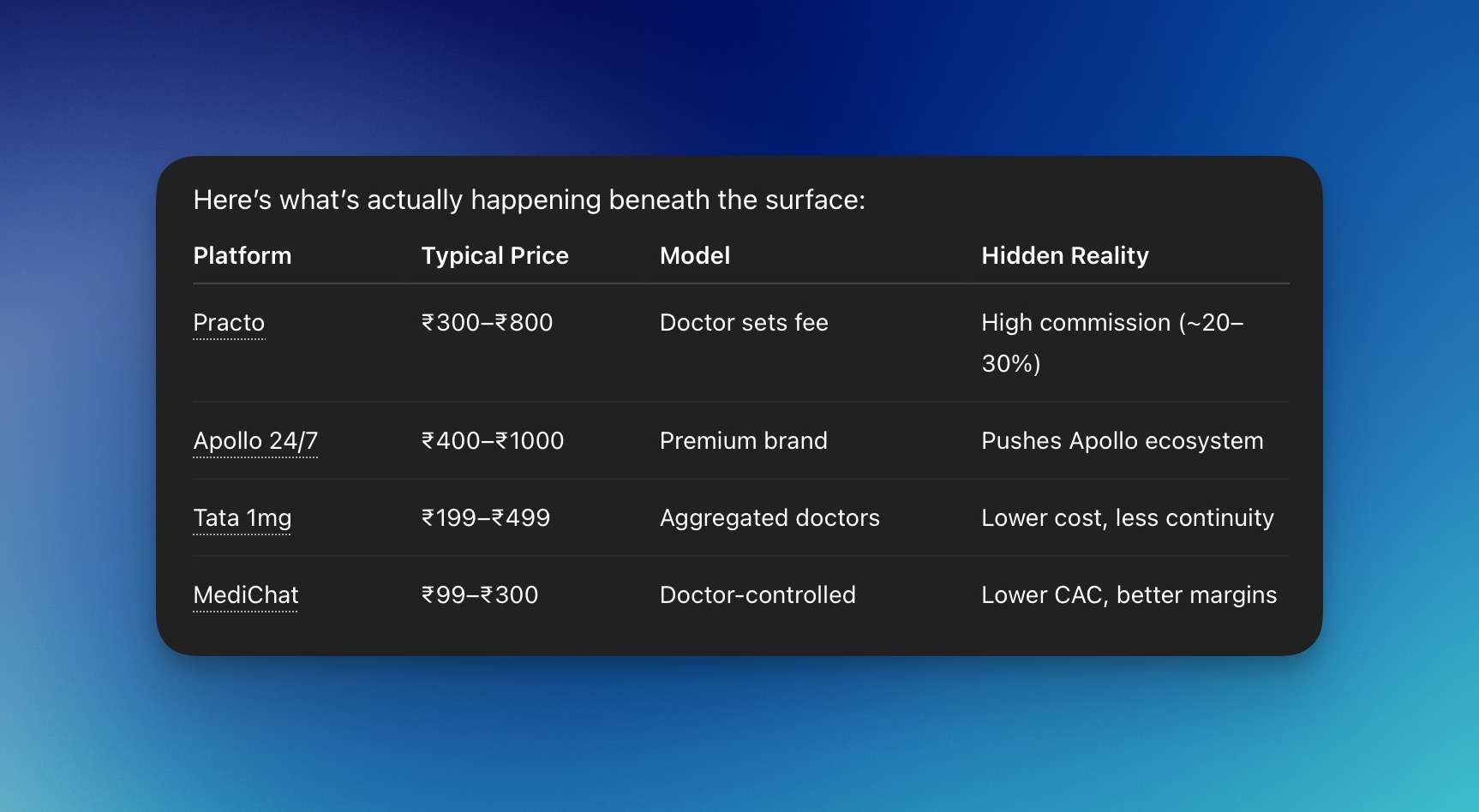

Pricing breakdown across platforms (Practo vs Apollo vs others)

Practo charges around ₹300 to ₹800 rupees, and in this model, the doctor usually sets the consultation fees. There is a high commission of about ₹20 to ₹30 percent, which acts as a hidden cost in the Practo marketplace.

Apollo 24/7 usually charges in the range of ₹400 to ₹1000 rupees. This model positions itself as a premium brand because it promotes the Apollo ecosystem, including its hospitals and pharmacy. The hidden cost is that it pushes users deeper into the Apollo 247 ecosystem.

Tata 1MG charges around ₹200 to ₹500 rupees for doctor consultations. It follows an aggregated doctor model. While the cost is relatively low, continuity is also low.

Coming to Medichat.in, the typical cost is around ₹99 to ₹300 rupees, which is among the lowest in the online telemedicine marketplace in India. The business model is controlled by doctors, and it has a low customer acquisition cost as well as better margins.

One key insight to note is that price is not about doctor value. It is about recovering customer acquisition cost. Since most platforms rely on ads and spend heavily to acquire users, the same doctor may be priced at ₹300 rupees on one platform and ₹700 rupees on another. Platforms inflate pricing to sustain ad spending.

Where most platforms fail (hidden fees, delays, doctor quality)

Let's be honest. Doctor quality on large aggregator platforms is inconsistent. There is no strong standardization or structure in place, and ratings are often inflated or gamed. From interviews with doctors, it has been observed that on some platforms, patients can leave reviews even if they have not actually consulted the doctor. This leads to misleading profiles.

On the other hand, platforms like Medichat.in follow a more controlled approach, where a doctor can only be reviewed by a patient who has actually consulted them. This usually requires uploading a recent prescription, not older than three weeks, and verification by the doctor before it becomes visible to others. This helps build trust in the system.

There is also the issue of delayed response times. Even though some applications claim to offer instant consultations, in reality, wait times can range from fifteen to forty minutes, especially during peak hours.

Over commercialization is another problem. Doctors and platforms often push lab tests and medicines, many of which may not always be necessary. In platforms where everything operates within the same ecosystem, medicine margins may be prioritized, increasing costs for patients.

There is zero continuity of care in many cases. Each consultation is often with a new doctor, and patient history is not deeply tracked or utilized. Compliance concerns, such as those related to HIPAA, make platforms cautious about storing and managing sensitive data, which further limits continuity.

There is also platform dependency risk for doctors. They do not truly own their patients and are effectively renting access through these platforms.

One important point is that founders building another telemedicine marketplace app may find that retention is broken on both sides, for both doctors and patients.

Who should use it vs who should not

So finally, it comes down to the question of who should use it and who should not. There is a good fit and a bad fit for each telemedicine application.

Good fit

- Mild infections, cold, fever

- Follow ups

- Prescription refills

- Tier 2 and Tier 3 access gaps

Bad fit

- Complex diagnosis cases

- Physical examination dependent conditions

- Emergency care

It is clear that telemedicine in India is still triage first, not diagnosis first.

Contrarian: Why most telemedicine apps are overpriced

Most people think that 300 rupees is cheap, but it is not. Especially in India, the cost of acquisition is high. It is usually between 150 to 400 rupees per user through Google Ads. On top of that, there is platform commission and brand marketing overhead. So there is a high chance that the patient is paying 50 percent more than what they would have paid if they had consulted a nearby doctor instead of using an online consultation application.

A patient may pay 500 rupees, while the doctor gets only around 250 to 350 rupees. The rest goes into platform economics. This is where the mismatch happens. The consultation itself is not expensive, the distribution is very expensive.

Why affordability will win the next decade

The future of the Indian healthcare ecosystem is not premium, it is volume driven and affordability first. What is likely to win includes ₹50 to ₹150 rupees consultation models, subscription based primary care, doctor owned micro brands, and a WhatsApp first care layer. The reason is simple. India is price sensitive, not convenience sensitive. Trust beats UI, and continuity beats discoverability.

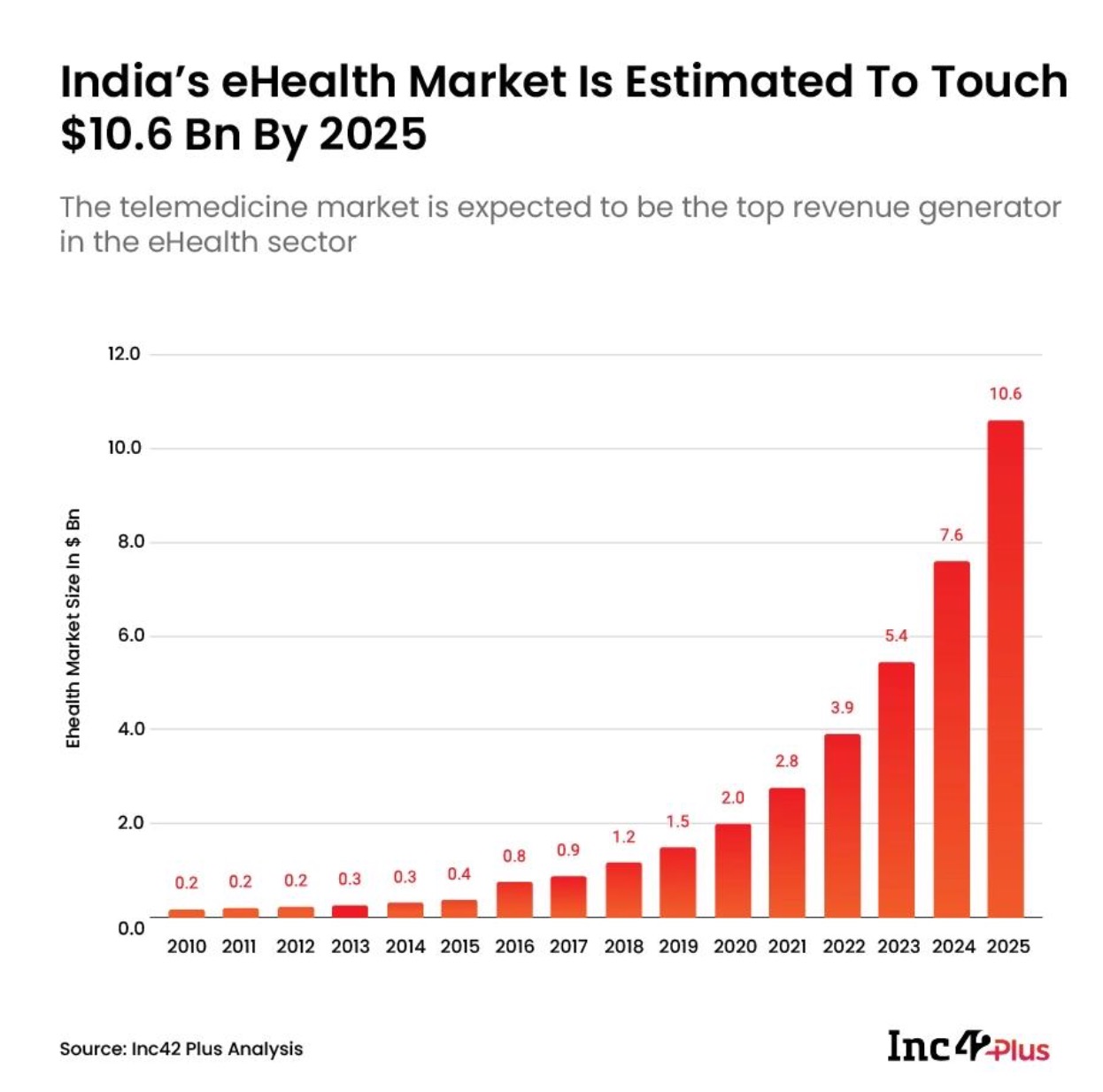

According to Inc42 Plus analysis, India's eHealth market is estimated to reach $10.16 billion dollars by 2025, where telemedicine is expected to be the top revenue generator in the eHealth sector. Based on past trends, there was limited growth before 2025. The early spike began around 2016 with initial digital adoption and infrastructure push. After 2025, the market shows a sustained 35 to 40% CAGR.

The real story is not the early years. The real signal is that telemedicine in India has entered a compounding phase after 2020. We are likely to see around 40% year on year growth. The market is expanding fast, but it is also getting crowded just as quickly.

Share this article

Rittam Debnath, FOUNDER

Rittam is the founder of Medichat, building AI-powered communication tools for private doctors in India. He writes about the future of digital healthcare, clinical workflow automation, and what it actually takes to build infrastructure for independent medical practices at scale.

Try MediAI Free for 14 Days

Built for Indian private practitioners. No credit card required. Doctor approval on every message.